OrbitX vs Betfair: Sports Betting Exchange at 40% Less Commission

OrbitX is a Betfair white label sports betting exchange. Same liquidity, same football and tennis markets, 3% commission instead of 5–7%.

What is OrbitX?

OrbitX is a sports betting exchange: a platform where you bet on football, tennis, and other sports against other users rather than against a bookmaker. Like Betfair, it operates on a back/lay model: you can back a team to win (bet that it will happen) or lay a team (bet that it will not happen), taking the opposite side of someone else's bet. This peer-to-peer structure eliminates the bookmaker's margin entirely. The exchange makes its money by charging commission on your net winning profits.

What makes OrbitX distinctive is that it is a Betfair white label. This means it is not an independent exchange with its own small liquidity pool. It connects directly to Betfair's order book - the largest betting exchange in the world. When you place a bet on OrbitX, it is matched against the same pool of orders that Betfair users see. The liquidity, the market depth, and the available prices are identical.

The difference is in the terms. OrbitX, accessed through Asianconnect, charges a flat 3% commission on net profit. Betfair's standard rate is 5%, and it can go as high as 7% depending on your market and activity level. The exchange experience is the same - the commission you pay for it is substantially lower.

Same liquidity, different commission

This is the point that matters most, so let's be absolutely clear about it: OrbitX is not a separate, smaller exchange that happens to look like Betfair. It is Betfair. The underlying technology, the matching engine, and the order book are Betfair's. Every order placed on OrbitX enters the same pool as every order placed on Betfair.com, Betfair's mobile app, and every other Betfair white label worldwide.

This means there is no liquidity trade-off. You are not accepting thinner markets in exchange for lower commission. The markets are identical. The prices are identical. The matched volume is identical. The only variable that changes is the percentage taken from your winning bets.

For context, Betfair's exchange typically sees over £100 million matched on a single Premier League weekend. OrbitX users are trading into that exact same pool. Whether a market shows 50,000 or 5 million in available liquidity, it is the same number you would see logged into Betfair directly. The 3% commission advantage becomes especially significant when you start systematically exploiting price gaps between sharp books and the exchange. We explain that approach in detail in our value betting strategy guide.

The 3% advantage explained

Exchange commission is charged on your net profit from winning bets, not on your stake. This is a crucial distinction that new exchange users sometimes misunderstand. If you place a €1,000 back bet at odds of 2.00 and it wins, your gross profit is €1,000. The commission is calculated on that €1,000 profit:

On a single bet, the €20 difference seems modest. But exchange trading is a volume activity. Professional exchange users place hundreds of trades per month, and the commission difference compounds rapidly. A trader generating €10,000 per month in net profit saves €200 per month, €2,400 per year, purely from the commission reduction. At €50,000 monthly profit, the annual saving is €12,000.

Importantly, when you lose a bet on the exchange, you pay zero commission. Commission only applies to net winning markets. This is the same on both Betfair and OrbitX. The difference is purely in the rate applied to your profits.

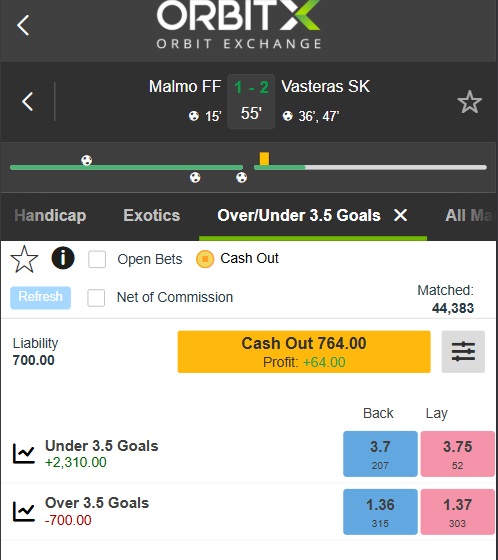

Cash Out: same feature, lower cost

Cash Out is one of the most-used features on any betting exchange. It lets you settle a bet before the market closes - locking in a guaranteed profit if your position is winning, or cutting your losses if it has moved against you. The exchange calculates the current value of your bet from live back and lay prices and offers you a single-click exit.

Because OrbitX runs on Betfair's order book, the Cash Out function is identical to the one Betfair users are familiar with. The same calculation, the same price feed, the same partial Cash Out option for taking a portion of your position off the table while leaving the rest running. There is no version compromise here - it is the same tool, accessed through a different wallet at 3% commission instead of 5–7%.

For in-play bettors and traders who frequently exit positions before settlement, Cash Out is not optional - it is core to how the exchange is used day to day. OrbitX delivers it without modification.

How much would you save?

Use the slider below to see the commission difference based on your typical monthly exchange profit:

Full feature comparison

The following table compares Betfair direct and OrbitX via Asianconnect across every dimension that matters to an exchange trader:

Who benefits most from switching?

Pre-match exchange traders

If you trade football, tennis, or horse racing markets before kick-off, backing at higher odds and laying at lower odds (or vice versa) to lock in a profit regardless of the outcome, you are generating frequent small profits on which commission eats significantly. At 5%, a €50 green-up becomes €47.50. At 3%, it becomes €48.50. Over 200 trades per month, that extra €1 per trade is €200/month you are currently giving to Betfair.

Arbitrage operators

Arbitrage between a sportsbook and an exchange is one of the most common professional strategies. You back on a bookmaker at high odds and lay on the exchange at lower odds, pocketing the difference. The exchange commission directly reduces your arbitrage margin. At 3% instead of 5%, every arbitrage opportunity becomes 2 percentage points more profitable, and opportunities that were previously too thin to be worth executing become viable.

With Asianconnect, this is particularly powerful because PS3838 (your sportsbook) and OrbitX (your exchange) share the same wallet. You do not need to transfer funds between accounts to execute an arb - the capital is already in both places simultaneously.

Matched bettors

Matched betting relies on laying bets on the exchange to eliminate risk from free bet promotions. Every lay bet on a winning outcome incurs commission, which directly reduces your matched betting profit. Reducing commission from 5% to 3% improves your yield on every single free bet you process.

In-play traders

Live trading, entering and exiting positions during a match based on game flow, generates high volumes of small profits. Commission is the single largest cost for an in-play trader, often exceeding any other expense. The 2 percentage point reduction from 5% to 3% represents a 40% cut in your operating costs.

Betfair Premium Charge payers

If you are a consistently profitable Betfair user, Betfair may apply the Premium Charge, an additional fee that can take your effective commission rate above 20% of net profits. OrbitX does not apply a Premium Charge equivalent. For traders already subject to this penalty, the move to OrbitX is not a marginal improvement - it is a fundamental restructuring of their cost base.

How to access OrbitX

OrbitX is not available as a standalone platform. You access it through a betting broker, specifically through Asianconnect. The process is straightforward:

For a complete walkthrough of the Asianconnect platform, including PS3838 sportsbook access, payment details, and payout timelines, read our full Asianconnect review.